在投資/交易中,「尾部」一詞指的是機率分布的極端區域,代表發生機率低但可能對投資回報產生重大影響的結果。例如,「肥尾」是指機率分布中極端事件的機率高於正常分布所預期的機率。這意味著極端事件發生的可能性其實遠高於投資者的預期,投資者應該為這些罕見但潛在重大的事件做好準備。

換句話說,尾部是機率分布中的極端結果,可能會對股市產生巨大影響。以下是一些真實的股市例子:

1. 2020年初爆發的新冠疫情是一個尾部事件。股市在疫情開始時迅速下跌,因為投資者擔心疫情將對全球經濟帶來嚴重影響。

2. 2008年的金融危機也是一個尾部事件。它的發生可能性被低估了,導致市場崩潰。許多金融機構倒閉,股市也崩盤。這個事件後來成為了市場上一個非常重要的教訓,讓投資者更加重視尾部風險。

3. 道瓊斯指數的單日下跌也是一個尾部事件。例如,1987年的黑色星期一,道瓊斯指數一天內下跌了22.6%。這種劇烈的波動是相當罕見的,但卻對投資者產生了極大的影響。

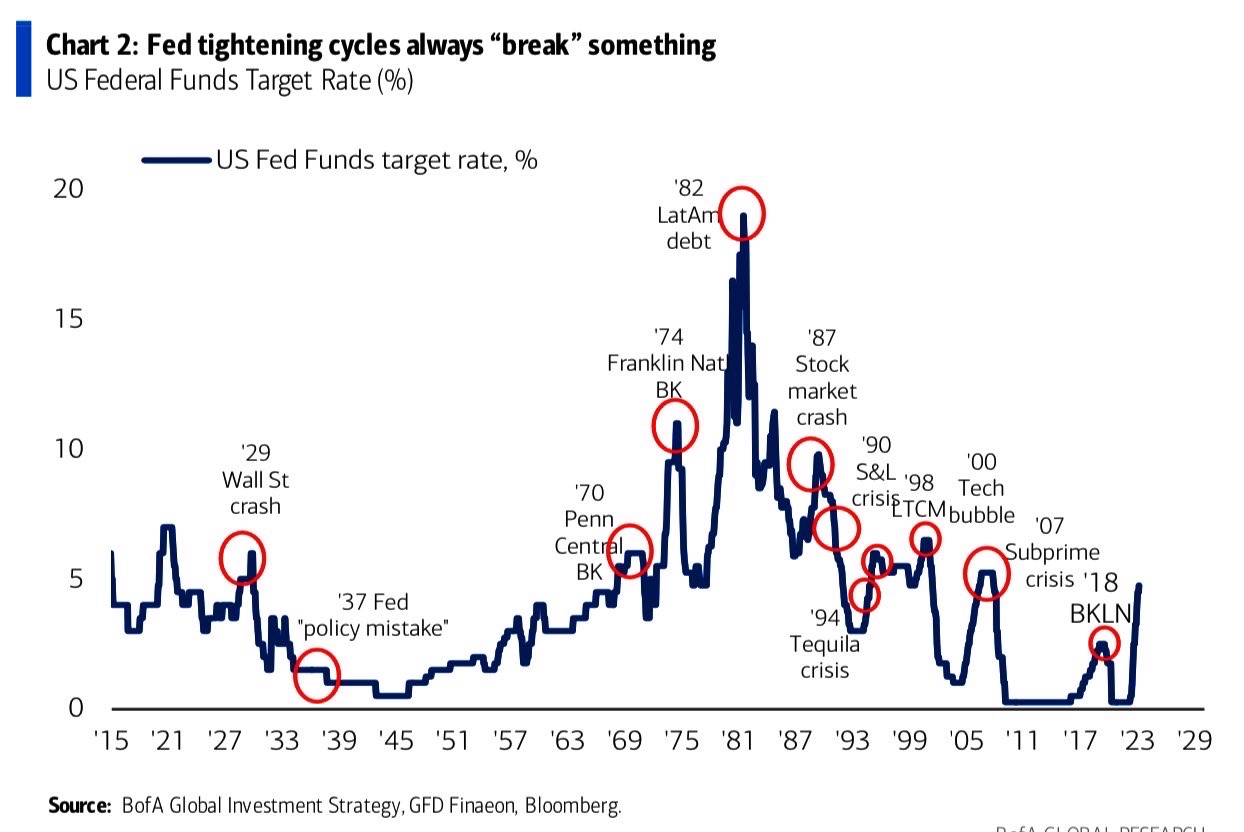

這些事件的發生機率很低,但它們對股市和投資組合產生的影響可能非常大。現時聯儲局認為美國經濟將出現軟着陸,便正正是無視尾部風險的存在。其實每次聯儲局收水,都會令尾部風險大升!

In investing/trading, the term "tail" refers to the extreme ends of a probability distribution. It represents the low-probability outcomes that are unlikely to occur, but can have significant impacts on investment returns if they do.

For example, a "fat tail" refers to a probability distribution where the probability of extreme events is higher than what would be expected from a normal distribution. This means that extreme events are more likely to occur, and investors should be prepared for these rare but potentially significant events.

Tail risk is the risk of losses due to extreme events in the tail of the distribution. Investors use tail risk measures to evaluate the probability and potential impact of these events on their investments. By assessing tail risk, investors can implement risk management strategies to mitigate the potential impact of these events on their portfolios.

Here are some research paper references on tail risk published by prestigious publications:

1. "Tail Risk and Asset Prices" by Tobias Adrian and Markus K. Brunnermeier, published in The Review of Financial Studies in 2016.

2. "Tail Risk in Hedge Funds: A Unique View from Portfolio Holdings" by Vikas Agarwal, Stefan Ruenzi, and Florian Weigert, published in The Review of Financial Studies in 2017.

3. "Global Tail Risk and Expected Equity Returns" by Lubos Pastor and Robert F. Stambaugh, published in The Journal of Finance in 2012.

4. "Dynamic Tail Risk Premia and the Forecasting Performance of Option-Based Indicators" by Tim Bollerslev, Viktor Todorov, and Lai Xu, published in The Journal of Econometrics in 2018.

5. "Tail Risk and the Limits of Diversification" by Nick Baltas and Robert Kosowski, published in The Journal of Portfolio Management in 2016.

These research papers provide valuable insights into tail risk and its impact on investment returns. They have been published in highly regarded finance and economics journals, indicating their significance in the field of finance.

重要聲明:股市漁夫內的所有內容,包括本影片,絕不構成任何投資意見或購買任何股票及金融產品的特定推薦意見及/或不構成任何游說或要約,以購買、出售或以其他方式交易任何證券、期貨、期權或其他金融工具或其他產品,漁夫系統的內容亦並非就任何個別投資者的特定投資目標、財務狀況及個別需要而編製。投資者不應只按漁夫系統的內容進行投資。用戶必須留意,漁夫系統的所有訊號,並非是買賣訊號或任何投資建議,而所有訊號均是全自動用第三方提供之客觀市場數據計算出來的結果,當中並不涉及任何人為的想法、修改、修訂或任何投資建議。本網站包含的所有內容、資訊、訊號,並不針對任何特定的投資目標、財務狀況以及可能使用或接收該內容的特定人員的特定需求。在作出任何投資決定前,投資者應考慮各種金融產品的個別特點、個人的投資目標、可承受的風險程度及其他因素,並適當地尋求獨立的財務及專業意見。

詳情請重溫股市漁夫FAQ及免責聲明。

最後更新: 2023-02-21